HECM Line of Credit

A Powerful Retirement Planning Tool

For homeowners 62+, the HECM line of credit can provide flexible, tax-efficient* access to home equity, a growing reserve for future needs, and a smarter way to strengthen retirement income.

What Is a HECM Line of Credit?

A HECM (Home Equity Conversion Mortgage) is the FHA-insured reverse mortgage program for homeowners age 62 and older. When structured as a line of credit, it allows you to convert a portion of your home equity into flexible borrowing power, available when and if you need it.

With a HECM line of credit, you can:

- Access a principal limit based on age, home value, and interest rates

- Leave some or all of those funds in a flexible line of credit

- Draw only what you need, when you need it

- Repay voluntarily and restore future borrowing capacity

- Eliminate required monthly mortgage payments while still living in the home**

**Borrowers must continue paying property taxes, homeowners insurance, HOA dues (if applicable), and maintain the home.

What Is a HECM Line of Credit?

A HECM (Home Equity Conversion Mortgage) is the FHA-insured reverse mortgage program for homeowners age 62 and older. When structured as a line of credit, it allows you to convert a portion of your home equity into flexible borrowing power, available when and if you need it.

With a HECM line of credit, you can:

- Access a principal limit based on age, home value, and interest rates

- Leave some or all of those funds in a flexible line of credit

- Draw only what you need, when you need it

- Repay voluntarily and restore future borrowing capacity

- Eliminate required monthly mortgage payments while still living in the home**

**Borrowers must continue paying property taxes, homeowners insurance, HOA dues (if applicable), and maintain the home.

Why the HECM Line of Credit Is Different

Unlike a traditional HELOC (Home Equity Line of Credit), the HECM line of credit was designed with retirement in mind.

Unused Credit Can Grow

Your available borrowing power can increase over time, even if home values stay flat.

No Required Monthly Mortgage Payments

As long as program obligations are met, there are no required monthly mortgage payments.

Interest Only on What You Use

You only pay interest on funds you actually borrow.

Flexible Prepayments

Make voluntary payments anytime to reduce your balance and restore borrowing power.

Non-Recourse Protection

You or your heirs will never owe more than the home is worth when the loan is repaid.

Built-In Emergency Reserve

Create a standby resource for health costs, repairs, caregiving, or unexpected expenses.

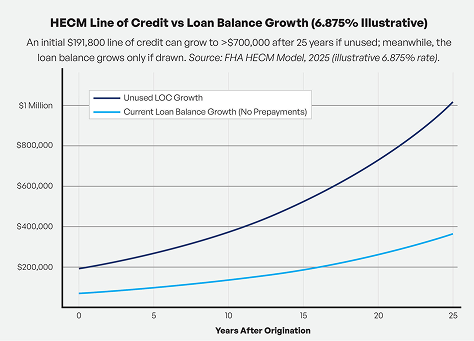

A Line of Credit That Can Grow Over Time

One of the most powerful features of the HECM line of credit is that unused borrowing capacity can grow automatically over time. On an adjustable-rate HECM, your available line of credit increases at the same effective rate charged on the loan balance (index + margin + FHA mortgage insurance). That growth compounds month over month and is not dependent on home appreciation.

In simple terms:

The earlier a HECM line of credit is established, the more future borrowing power it may create even if you never touch it today. This makes the HECM LOC a unique retirement reserve: one that grows independently of market performance and can help provide future flexibility when it matters most.

This illustration shows how an unused HECM line of credit can grow over time compared with loan balance growth when funds are used. It’s one of the most misunderstood, and most valuable features of the HECM strategy.

Voluntary Payments Can Increase Future Borrowing Power

One of the most overlooked advantages of the HECM line of credit is how voluntary payments can restore borrowing capacity. When you make an optional payment, your total loan balance is reduced. Because your available line of credit is calculated as your principal limit minus your loan balance, reducing that balance increases your available credit dollar-for-dollar.

$50,000 balance + $5000 voluntary payment=$55,000 line of credit

If your HECM balance is $50,000 and you make a $5,000 voluntary payment, your available line of credit can increase by that same $5,000. That means optional repayments can help restore borrowing power, improve flexibility, and strengthen your long-term retirement reserve.

Real-World Ways to Use a HECM Line of Credit

- Emergency expenses

- Home repairs & modifications

- Health care/caregiving costs

- Tax-efficient income coordination

- Delaying Social Security

- Market downturn protection

- Aging in place improvements

*Consult your tax professional. HECM proceeds are generally loan advances from home equity, not taxable income.