Turn Home Equity Into a

Smarter Retirement Strategy

Wealth Advantages of a Reverse Mortgage

Creating more flexibility, more stability, and peace of mind.

For many retirees, their home is their largest asset, but it’s often the least utilized in a retirement plan. A Home Equity Conversion Mortgage (HECM), also known as a reverse mortgage, can help homeowners 62+ turn that untapped equity into a flexible financial tool designed to support long-term retirement confidence.

A reverse mortgage isn’t about replacing your savings or investments. It’s about coordinating your home equity with the rest of your retirement strategy to create more flexibility, more stability, and more peace of mind.

Creating more flexibility, more stability, and peace of mind.

For many retirees, their home is their largest asset, but it’s often the least utilized in a retirement plan. A Home Equity Conversion Mortgage (HECM), also known as a reverse mortgage, can help homeowners 62+ turn that untapped equity into a flexible financial tool designed to support long-term retirement confidence.

A reverse mortgage isn’t about replacing your savings or investments. It’s about coordinating your home equity with the rest of your retirement strategy to create more flexibility, more stability, and more peace of mind.

The Opportunity

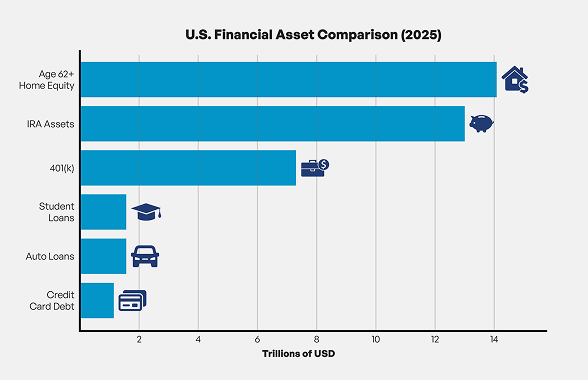

Across the United States, homeowners age 62 and older are sitting on more than $14 trillion in home equity, a record-high source of wealth that is often overlooked in retirement planning. For many retirees, home equity represents 30–50% of total net worth, yet it’s rarely used as part of a broader financial strategy.

Instead, many households rely only on traditional retirement assets like:

- Savings

- Investment accounts

- IRAs and 401(k)s

- Social Security

Meanwhile, one of their largest assets remains untouched.

This creates a common set of retirement concerns:

- Will my money last as long as I do?

- What happens if the market drops early in retirement?

- How do I cover unexpected medical or long-term care costs?

- How can I preserve my investments while still maintaining income?

A reverse mortgage can help answer those questions by transforming home equity into a strategic source of liquidity.

A More Coordinated Retirement Plan

A reverse mortgage is not a loan of last resort. When used strategically, it can strengthen a retirement plan by working alongside your other assets, not against them.

By coordinating home equity with savings and investments, retirees can:

- Improve monthly cash flow

- Reduce pressure on investment withdrawals

- Create a backup source of funds during market volatility

- Preserve portfolio value during downturns

- Extend the life of retirement assets

- Increase confidence in long-term planning

This coordinated approach helps retirees stay flexible and better prepared for life’s financial uncertainties.

How a Reverse Mortgage Supports Wealth Preservation

The goal of a reverse mortgage isn’t to replace traditional retirement assets, it’s to help protect them.

When markets fluctuate, many retirees are forced to sell investments at the wrong time just to maintain income. That can create long-term damage to a portfolio, especially early in retirement. A reverse mortgage line of credit can help solve that problem. Instead of drawing from investments during a down market, homeowners can temporarily access home equity to cover expenses. This allows retirement accounts more time to recover and reduces the impact of sequence-of-returns risk.

This strategy can help retirees:

- Stay invested during market downturns

- Avoid selling assets at a loss

- Reduce portfolio stress

- Preserve future growth potential

- Maintain income consistency in retirement

Key Financial Planning Advantages

A reverse mortgage can be used in several ways to support a stronger retirement strategy

Increase Cash Flow

Eliminate required monthly mortgage payments to free up more income for everyday expenses.

Create a Growing Line of Credit

Establish a standby line of credit that grows over time and can be accessed when needed.

Protect Investment Accounts

Use home equity during market downturns instead of selling investments at depressed values.

Cover Major Expenses

Fund healthcare costs, home updates, or other large expenses without draining retirement savings.

Improve Tax Flexibility

Reverse mortgage proceeds are generally not considered taxable income, offering added planning flexibility.

Support Legacy Planning

Preserve other liquid assets for heirs, charitable giving, or long-term estate goals.

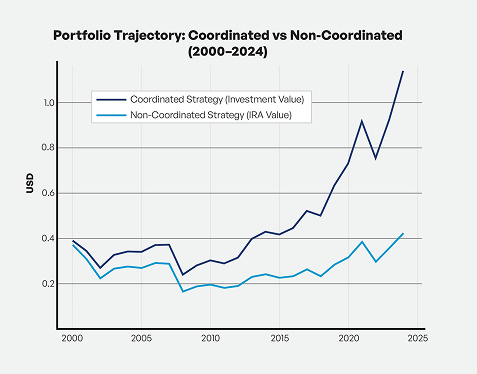

Coordinated vs. Non-Coordinated Planning

A traditional retirement strategy often relies solely on portfolio withdrawals. That means when the market declines, retirees may be forced to sell investments at a loss, reducing future growth potential and increasing portfolio risk. A coordinated strategy adds another layer of flexibility.

By using home equity as a reserve source of income, retirees gain the ability to:

- Control when they tap investments

- Maintain more consistent income

- Reduce exposure to market volatility

- Preserve long-term portfolio growth

- Stay on track through changing market conditions

A coordinated plan doesn’t replace the retirement strategy you already have. It helps protect it.

Why It Matters

For many retirees, home equity is more than just wealth tied to a house, it’s a financial resource that can create stability, flexibility, and confidence throughout retirement.

When used thoughtfully, a reverse mortgage can help transform home equity into a strategic retirement asset that supports:

- Sustainable income

- Greater financial resilience

- Improved retirement confidence

- Better protection for long-term wealth